From inflation and supply chains to climate change and housing prices, we explore how things could unfold, with help from an expert panel

Well, that wasn’t always so fun. As they put 2021 behind them, with the COVID-19 pandemic still very much alive, business decision makers face another challenging year. What’s coming our way in 2022? To tease out some key themes for B.C. organizations of all sizes, we assembled a panel of seven experts.

Of course, it wouldn’t be a business and economic outlook without a big disclaimer. Several of the interviews with our panel took place before the floods that brought so much destruction, as well as the arrival of the Omicron variant. Here’s hoping for a better 2022.

Our panel of experts

Ryan Berlin, senior economist and director of intelligence, Rennie Intelligence

John Davis, senior vice-president and regional manager, commercial banking, B.C. region, Wells Fargo

Fiona Famulak, president and CEO, BC Chamber of Commerce

Alex Hemingway, senior economist and public finance policy analyst, Canadian Centre for Policy Alternatives

Ken Peacock, chief economist and senior vice-president, Business Council of British Columbia

David Williams, vice-president of policy, Business Council of British Columbia

Bryan Yu, chief economist, Central 1 Credit Union

22 things you need to know about B.C. business and the economy in 2022

1. The big picture is mixed

Several forces are converging to deny B.C. and the rest of the world a smooth COVID recovery. “The economy is improving because the pandemic is ebbing and the economy is reopening,” says David Williams of the Business Council of B.C. “But we are running into some headwinds and difficulties with supply chains and global supply.” So the outlook for global and Canadian economic growth has been downgraded for 2022, with some of that expansion pushed back to 2023. “At the same time, inflation has ended up being far higher, broader and more sustained than many central banks had projected.”

2. An economic rebound hides fundamental flaws

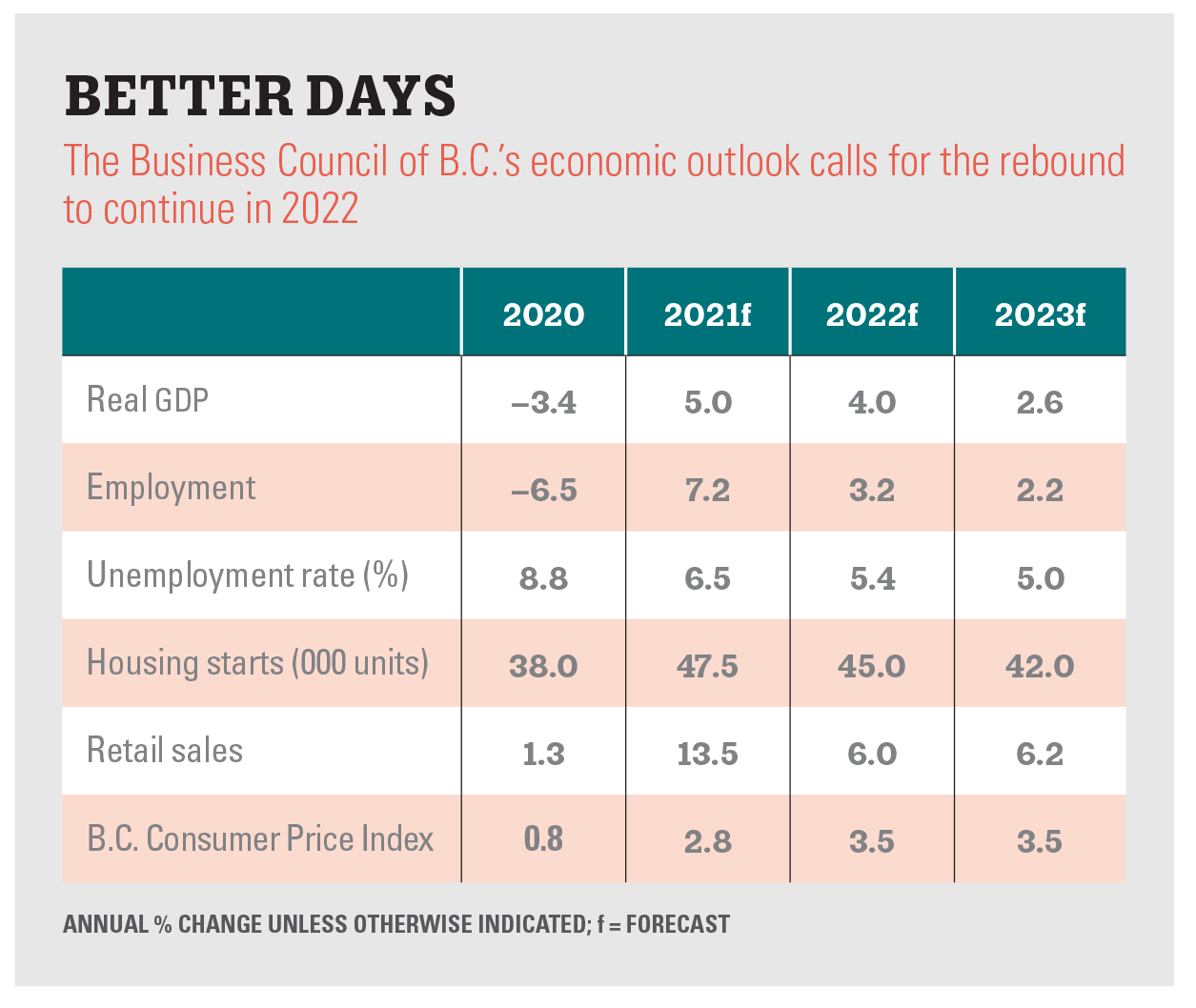

As of December, the BCBC forecast the province’s real GDP growth at 5 percent for 2021 and 4 percent this year, versus 4.3 percent for Canada as a whole. Still, the economic fundamentals are much softer than those relatively strong numbers suggest, Ken Peacock stresses. “If you look across different industry sectors, for nine of the 16 broad industry categories, employment levels are still below pre-pandemic levels,” he says of B.C. “So more than half the industries have not seen jobs recover to where they were, and we’re almost two years out now.”

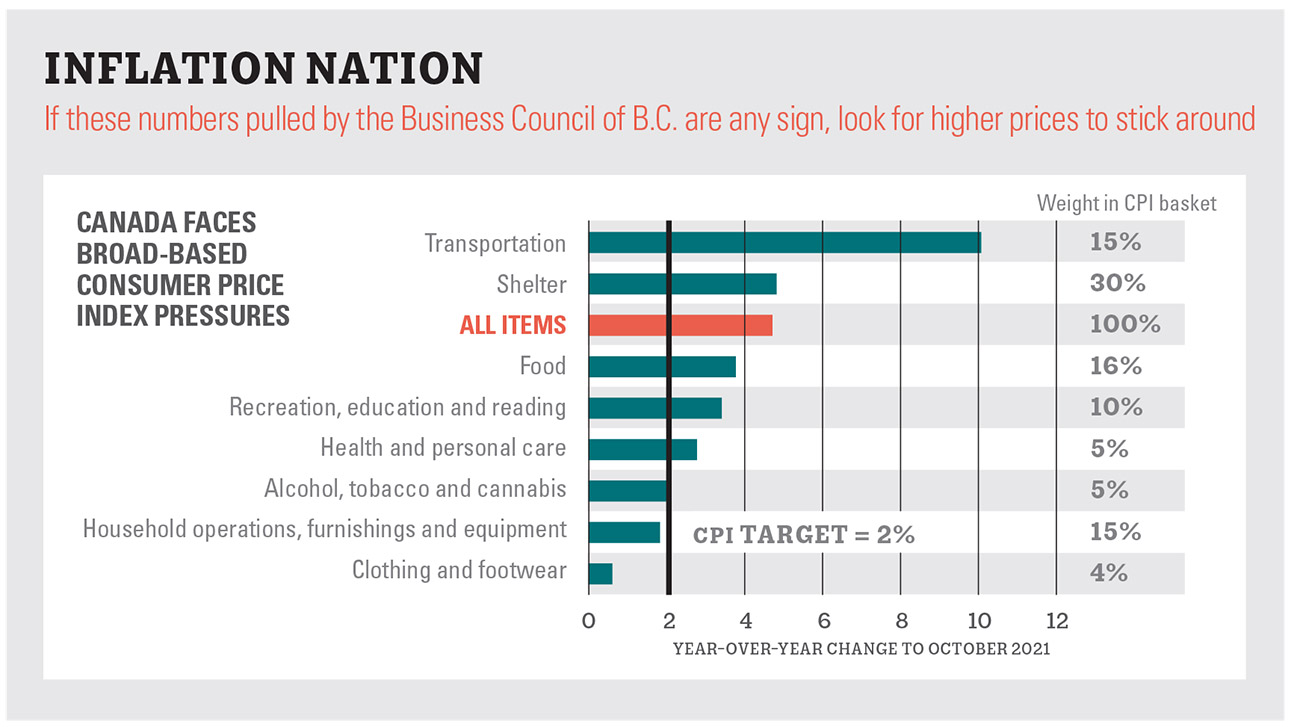

3. Inflation looks like it‘s here to stay

Anyone convinced that the current wave of inflation is a passing phase could be disappointed. After the Bank of Canada upgraded its year-average inflation forecast by a full percentage point, Williams says, the Consumer Price Index (CPI) rose 4.7 percent year-over-year in October. “So these are very difficult times for Team Transitory.”

With inflation not expected to return to 2-percent levels until 2024, Peacock holds out hope that higher prices will ease somewhat. “But if we see 5-, 5.5-, 6-percent inflation stick around for two or three or four years, purchasing power is going to be severely eroded,” he says. “Households will fall behind. And this, I think, is a potential problem for this provincial government, which, from the day it was elected, has been very interested in raising well-being and prosperity for households, personal incomes.”

4. Interest rates have nowhere to go but up

Uncomfortably high inflation means that businesses should plan for rising interest rates, says Central 1’s Bryan Yu. He thinks the market’s call for three rate increases this year and two in 2023 is aggressive, though, given that the economy isn’t fully healed. “It’s heading in the right direction, but whether that warrants three hikes is debatable.”

In real terms after inflation, Williams notes, Canada’s policy interest rate is 4.5 percent. “Interest rates affect the economy with a lag of about two quarters to six quarters,” he says. “So you’ve got to ask whether a real policy rate of 4.5 percent is what the economy really needs in six to 18 months. It doesn’t look like it needs that kind of stimulus.”

With real interest rates at an all-time low, the Bank of Canada has promised not to change the policy rate until the second half of 2022. “With inflation now at 4.7 percent, it’s very difficult to believe that the central bank will leave interest rates on hold for that period of time,” says Williams, who points out that the BoC recently hinted at a second- or third-quarter hike. “But that still seems an awfully long time to leave interest rates, in real terms, being very significantly negative.” If real rates quickly move closer to zero, “that would be a very contractionary effect on the economy, and I don’t think the economy is all that strong and robust.”

5. Fintech could help save small business

The pandemic hasn’t been kind to smaller companies in need of financing. “Access to capital when you’re Jimmy Pattison is very different than if you’re some small business,” says Wells Fargo’s John Davis, whose firm typically provides loans and other services to companies with annual revenue north of $350 million. “And small businesses fell through the cracks a little bit here because they don’t have the access to capital that big companies have.”

As interest rates rise and labour constraints continue, those smaller outfits will face challenges in 2022, he predicts. Because the big Canadian banks have always had trouble figuring out that space, credit unions and other smaller financial institutions have tried to fill the gap, he says. But they want to move upmarket, too, because such loans don’t yield much of a return. “I’m wondering if some of the fintechs or non-bank solutions might be the ultimate credit providers and service providers to smaller businesses.”

6. Labour supply pains will continue, with a twist

“Without a doubt, the severe skilled labour shortage B.C. is experiencing is our biggest challenge in the next year,” the BC Chamber’s Fiona Famulak says. “There are jobs out there but not enough people to fill them. This is already impacting businesses and communities both large and small. In addition, the increasing cost of doing business and supply chain challenges are adding to the issues that small and medium-sized businesses are trying to manage.”

On the labour front, Davis has watched forest products companies hold job fairs to find mill workers. “One of our biggest clients is a hotel operator,” he says. “Getting people to do that kind of work is incredibly hard.” Davis attributes some of the shortage to the Canada Emergency Response Benefit (CERB), which made it relatively easy for workers with low-paying jobs to stay home. “It’s not just new people,” he says of the labour shortage. “It’s the people that have left and trying to get them to come back.”

At the same time, there’s still plenty of slack in the labour market, says Ryan Berlin of Rennie Intelligence. Before COVID, Metro Vancouver was home to 70,000 people looking for work—a number that has since grown to 100,000. “So there’s an excess of 30,000 people above what we had seen pre-pandemic who are wanting to work but can’t.”

Given that surplus, you’d think employers would have their pick, Berlin says. But even with Canada’s job vacancy rate at a record high, “they’re struggling to connect the skills and people out there to the needs that they have.”

7. Employment levels aren‘t what they‘re cracked up to be

Climbing out of what Peacock describes as a big hole, B.C. saw a 7-percent increase in jobs from January through October 2021, putting it ahead of the rest of the country. But distorting that picture is public sector employment growth, which spiked by about 16 percent, he notes.

And remember, employment throughout the province fell significantly in 2019, Peacock says. “So we went into the pandemic at a lower level of employment, which has made it much easier for B.C. to regain that pre-pandemic level of February 2020 that everybody’s been focused on.”

Peacock sees reason for concern about relatively muted hiring conditions in the private sector. “When I look at some of the additional costs that are being heaped on employers, going back to the employer health tax and then all these costs associated with managing the pandemic, some difficulties and challenges in hiring people and then sick-pay costs added on, one does wonder to what degree we’ll see stronger private sector hiring activity over the next couple of years.”

8. Expect supply chain woes to stretch on…and on

For B.C. businesses in a wide range of industries, global supply chain disruptions keep making it tough to serve their customers. “The view that they’ll soon sort themselves out seems a fairly optimistic assumption at this point,” Williams says of those troubles. “They look like they’re going to be around for quite some time.”

Just ask one of Wells Fargo’s biggest manufacturing clients, which recently announced that because it can’t get all the parts to fill its orders, it needs at least 18 months’ relief from the banks. “This is the market leader in North America for what they do, and they’re worried about that,” Davis says. Besides absorbing the cost of borrowing capital, the publicly traded company could see its market capitalization shrink, which makes it harder to borrow, he explains. Also, frustrated customers might look elsewhere—and a rival could step into the void. “That’s terrifying.”

9. Business investment is flagging—but there‘s hope

As the saying goes, you have to spend money to make money. But in Canada, business investment per worker has been falling for several years, according to recent research by the Toronto-based C.D. Howe Institute. “So we are becoming less industrialized—we have less capital equipment, less technology, less innovation, less research and development per worker than we did the previous year or five years ago,” Williams says.

Lately, with help from deep-pocketed foreign investors, several B.C. businesses have reached unicorn status. “But what matters for the country and what matters for real incomes across the country is what’s happening at the average firm,” Williams says. “At the average firm, there’s less investment per worker going on over time, and the capital stock is actually shrinking on a per-worker basis.”

Yu expects the tide to turn in B.C. “As businesses get more certainty in the market—they understand where the demand is, things are reopening and they’re not going to close—they are going to move back into reinvesting in their operations,” he says. Yu also thinks that given labour shortages, some companies will look at software and equipment to boost productivity. “Possibly they’ll have less of a need for as many employees.”

10. Either way, climate change will cost us

If there was ever any doubt, last year’s raging forest fires and catastrophic floods made it clear that climate change is a major threat to B.C. But not everyone is happy about our policy responses to this existential crisis. For his part, Peacock sees the provincial carbon tax adding to already soaring energy costs. “At the end of the day, the carbon tax in B.C. is going to hit consumers’ pockets, and it’s going to hit businesses as well.”

Companies with a domestic customer base can pass on those extra costs, Peacock adds. For exporters, though, there’s no such option. “Most of our big exporters, the ones that really matter, are not in a position to adjust their prices,” Peacock says.

Among jurisdictions with a price on carbon, B.C. is one of the few without a cap-and-trade system or other mechanisms to shield exporters, he explains. “Over time, what this means is a less productive export sector, and companies are going to be less willing to deploy capital and make investments in B.C., unless the policy framework is realigned,” Peacock says. “I think that weighs on the export sector over the next three, five, seven years here in B.C.”

For the CCPA‘s Alex Hemingway, high oil prices are yet another reason to move to renewables. “One of the issues that’s happening in terms of the lagging climate progress is the power of the fossil fuel industry,” he says, also citing lobbying efforts against employer-paid sick says and a wealth tax. “It gets at the power of these lobby groups to shape the policy agenda and throw some dirt in the gears when there’s a fear that it’s going to affect their interests.”

11. Like the rest of the world, we’ll keep an eye on China

To put economic pressure on other countries, an increasingly assertive China doesn’t hesitate to slow or halt imports, whether that’s Canadian canola or Australian coal. How vulnerable is B.C., given frostier-than-ever relations between Ottawa and Beijing?

In Wells Fargo’s local client base, the biggest single industry is forest products, which Davis calls the best example of a B.C. sector tied to China. “We’ve yet to hear—I’m touching wood as I say this—any concerns with that,” he says. “Are they going to be looking for that lumber supply from Russia? Are they going to be looking for it from Scandinavia? Maybe it’s too early for us to really see it, but I haven’t seen any fallout from that yet.”

12. As government supports wind down, businesses must find ways to add value

“Overall, pretty good,” the BC Chamber’s Famulak says when asked how we’re doing with government supports for businesses still navigating the pandemic. “But let me be clear: the federal and provincial governments need to look at ways they can continue supporting businesses that include easing tax burdens and slowing down the layering-on of costs as we have seen over the last few years. We need to deal with our skilled labour shortage, and governments need to explore all channels available to them, from enhancing immigration policy to essential skills training.”

Peacock suspects that many companies have been sustaining themselves on government programs. “When they’re wound down, we probably are going to see more businesses fail,” he says. “If these were struggling businesses, maybe shifting to another industry or sector or line of work will in the long term, in the medium term, be an improvement. But there’s pain associated with this turnover process.”

Williams suggests that businesses think about how to add value. “If they’re able to offer higher-value-added goods and services for their customers, they should do pretty well,” he says. “But the businesses that are in low-value-added sectors where they’re dependent on a low cost of labour and easy access to pools of low-cost labour, clearly that’s going to be more difficult.”

13. Land-based industries keep taking a hit

Peacock makes a distinction between the province’s tech sector, which is concentrated in Metro Vancouver and parts of Vancouver Island and the Interior, and land-based industries such as forestry and mining. For those businesses, the regulatory climate, Indigenous issues and the carbon tax make life complicated, he says.

Peacock singles out the provincial government’s recent announcement that it plans to defer logging on as much as 2.6 million hectares of old-growth forest. That policy decision could prompt the closing of 10 to 14 sawmills, plus a couple of pulp mills, he says. “This is going to lead to the shuttering and loss of high-value-added jobs.”

14. Indigenous economic reconciliation faces roadblocks

With the province and many businesses committed to economic reconciliation with Indigenous Peoples, what can we expect in 2022? “It’s mixed, because I think the reconciliation and economic development and First Nations’ involvement in economic projects is clearly a positive,” Peacock says. “And I think businesses have for many years been keen, as long as they know the rules and the relationship and who owns the land, to get on with doing business.”

But events like the blockade of the Coastal GasLink pipeline by a Wet’suwet’en Nation clan pose challenges, Peacock maintains. “I think it’s prompting companies to take a closer look at deploying hundreds of millions of dollars or half a billion dollars in the province and wondering what that investment return might be over a decade or two, given some of the complexities related to the land base.”

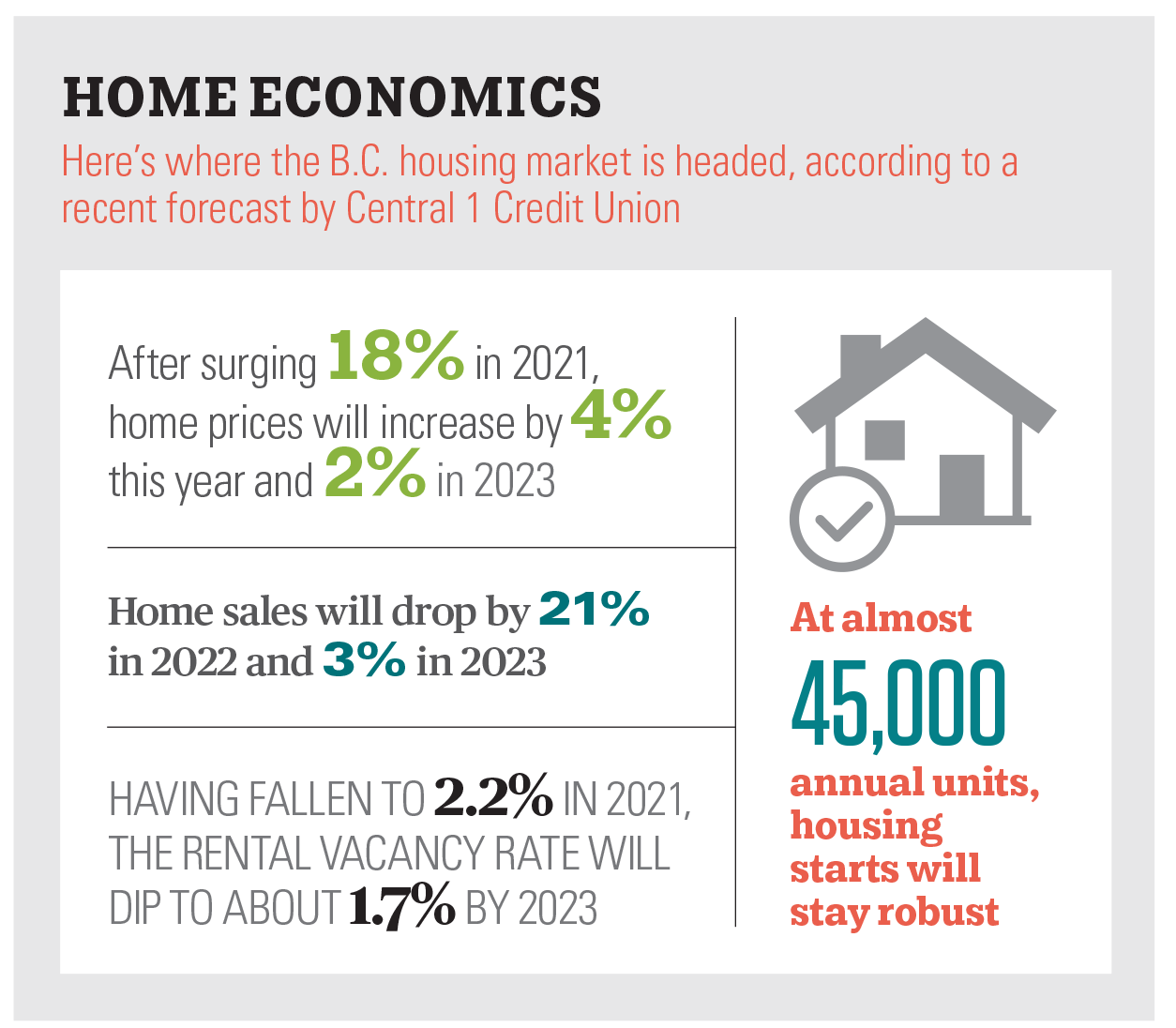

15. Dwindling choices spell more housing crisis

One of the biggest pandemic stories is the red-hot provincial housing market. With help from low interest rates, B.C. home sales remain well above pre-pandemic levels, Yu says. But for 2022, Central 1 forecasts a 21-percent drop.

Don’t expect prices to follow suit, though. “The pricing conditions are going to remain very strong because there’s no supply,” Yu says. “There’s not a lot of choice or options for a lot of buyers right now, so they’re kind of rushing toward the market.”

To tackle its shelter shortage, B.C. needs to massively increase not just public and not-for-profit housing but also the overall supply, the CCPA‘s Hemingway contends. “Every time we make a gain in another area—if people’s wages rise a little or if their costs go down for child-care investment—it can still quickly get eaten up by increased rents.”

READ MORE: Pandemic helps push Metro Vancouver home sales to record high in 2021

16. The COVID immigration boom could turn out to be a blessing

Rennie Intelligence’s Berlin was one of many observers left puzzled by the federal government’s pandemic immigration moves. At first, he was shocked to see Canada boost its target in the midst of COVID, given that it would inevitably result in a surplus of workers. The feds, who have set a quota of 1.2 million immigrants for 2021-23, welcomed some 220,000 during the first eight months of last year. So the year-end total could be an all-time high of 370,000.

For B.C., which gets about 14 percent of national immigration, that’s good news, Berlin maintains. Besides potential labour, he says, immigrants bring diverse cultures and perspectives. “So I think that bodes well for setting us up as we turn the corner and put COVID in our rear-view mirror.”

B.C. also stands to benefit from robust interprovincial migration, Berlin says. From April 2020 through last June, we attracted a net 43,000 new residents from other parts of the country while most other provinces lost people. “If you look at it from, again, a labour supply perspective, to me, that’s a good thing.”

With that population growth comes demand for new housing, Berlin adds. “Over the next six months, we’re not out of this, but I think there’s some tailwinds for our part of the world in particular that will put us in a pretty good position to begin to actually grow in the next year.”

17. For some, taxes remain a steep price to pay

Peacock doesn’t mince words about provincial taxes on people and businesses. “Top marginal tax rates are at a high for individuals,” he says. “Effective marginal tax rates on investment in B.C. are among the highest, if not the highest, in Canada. So it’s starting to shape up like the investment climate is pretty good for some industries, but it’s pretty bad for land-based operators and maybe some manufacturers here in B.C.”

18. Taxing the rich calls for getting creative

In Hemingway’s view, this is a good time to do something about growing economic disparity: “The public appetite for action in terms of reducing inequality, including taxing the rich, seems to be higher than at any point I can remember.” He cites a recent national survey by Ottawa-based Abacus Data in which 89 percent of respondents backed a 1-percent tax on the wealthiest Canadians to support pandemic recovery.

At the provincial level, Hemingway sees a big opportunity to redistribute wealth by taxing property, whose value in B.C. has climbed by more than $1 trillion since the mid-2000s. Today, property tax applies to individual parcels of land. “But now that we have the beneficial ownership registry online, what you could do is apply the tax to the total holdings of any specific landowner above a given value,” Hemingway says, suggesting that the provincial government use different brackets.

READ MORE: Tax the rich—well, the richest of them, anyway: report

19. Cities and the climate need more public transit

Post-pandemic and in an era of rising inequality and climate change, there’s a growing recognition the government must play a bigger role in several areas, Hemingway says. For example, B.C. needs to “massively and much more quickly invest in public transportation,” he argues. “We’ve been moving at a pace of maybe building about one SkyTrain line a decade in Metro Vancouver. If we’re serious about this climate thing and we’re also serious about city-building, we need to be looking at ramping that up considerably.”

20. Watch for a retail reconfiguration

At Central 1, Yu expects a B.C. retail slowdown this year, for two reasons. “No. 1, the sales numbers are being boosted by higher prices,” he says. The second factor: as the economy fully reopens, much of the demand related to housing should rotate back into services. “So we’ll see that in the GDP, but the retail numbers will suffer.”

During COVID, the property class that Wells Fargo has been most worried about is retail, Davis says. It remains a concern as shoppers keep moving online. Davis flags what he calls the barbell effect: big-box stores like Costco and Walmart are doing well, along with luxury retailers. “But if you’re in the middle category—if you’re the Gap or Old Navy or whatever it is—you’re getting slaughtered.”

However, experiences still matter, Davis says. Take Vancouver’s Robson Street, which now has less typical retail and more Asian-style service businesses such as tea shops and dessert spots. “I think you’re going to see a reconfiguration of retail in a big way.”

21. Natural resources have a big role to play in the recovery

Tech may grab all the headlines, but Williams contends that other sectors are better equipped to deliver us from the pandemic. “You really need your big economic engines to pull you out of this, and our big economic engines are the natural resources industries,” he says. “For every hour worked in the natural resources sector across Canada, we get $330 of value added.” In unconventional oil and gas, that number is $1,300—23 times the national average of $56.

Given their broader economic benefits, it doesn’t make sense to replace such industries with those that generate only $30 to $90 per hour worked, Williams says. “So it’s a really delicate balance, I think, for policy makers to address our carbon challenges but at the same time recognize Canada’s comparative advantages on international trade.”

22. As the economy rebounds, slow and steady might win the race

“We’re entering into a very delicate time in the economic recovery,” Williams says. “And so I think it’s important for the federal government, for central banks, also for the provincial government, to avoid any more policy mistakes,” he argues. “Change the game.” Although some government interventions in the economy were necessary, they might not be appropriate now, he adds. “And so we need to be a bit more nimble, I think.”

Still, Peaco