Bench Accounting’s Vancouver office

From bookkeeping to blockchain, Vancouver’s fintech stars are growing up and looking to go global

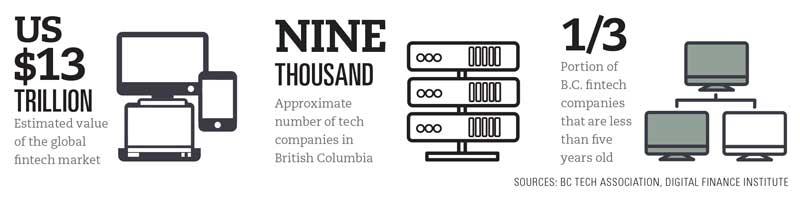

Call it Western financial alienation. With Canada’s big banks and traditional finance players headquartered in Toronto, perhaps it’s no surprise that B.C. is home to many of the country’s most promising and disruptive fintech companies. Backed by some sizeable investments, these businesses are shaking up the financial sector by using technology in novel ways. But this isn’t a new trend on the West Coast.

Fintech players such as Victoria’s Beanstream Internet Commerce Inc., along with online investment broker Qtrade Financial Group and payments company Tio Networks Corp., both headquartered in Vancouver, launched in the early days of the Web. All three were later acquired: U.S. giant PayPal Holdings Inc. bought Tio for $304 million last year, Beanstream was sold to U.S.-based Digital River Inc. and then Sweden’s Bambora in 2015, and Quebec’s Desjardins Group picked up Qtrade in 2013.

Now a fresh crop of B.C. fintech outfits are scaling up to make banking easier—and maybe turn the established financial world upside down. Here’s a sampling.

Sources: BC Tech Association, Listed Companies

BENCH ACCOUNTING

FOUNDERS: Ian Crosby (above), Jordan Menashy, Pavel Rodionov, Adam Saint

FOUNDERS: Ian Crosby (above), Jordan Menashy, Pavel Rodionov, Adam Saint

LAUNCHED: 2012

EMPLOYEES: 250

NICHE: Bookkeeping

ORIGIN STORY: UBC grads Crosby and Menashy founded Bench to tackle the problem of inefficient and time-consuming manual bookkeeping. With Rodionov and Saint, the pair got their company off the ground by landing a slot with famed New York incubator TechStars

INNOVATION: Bench offers subscription access to cloud-based software with in-house accountants taking care of all the bookkeeping. Small-business owners are freed up to keep working on their businesses and not in them

BANK RATING: Neutral. Bench has integrated with online e-commerce platforms including Gusto, Mindbody, Shopify and Stripe

CANADA DRIVES

FOUNDERS: Cody Green

FOUNDERS: Cody Green

LAUNCHED: 2010

EMPLOYEES: 400; expanding to the U.S. and U.K. in 2018

NICHE: Online lending

ORIGIN STORY: A former car salesman with a talent for web design, Green launched Canada Drives to turn around an inefficient auto financing industry. Rather than approve customers for a loan after they find the right car, he thought it should be the other way around

INNOVATION: Revolutionized access to auto financing in Canada by connecting customers and lenders through an online platform. Canada Drives collects basic customer data and sells the information to local car dealers

INNOVATION: Revolutionized access to auto financing in Canada by connecting customers and lenders through an online platform. Canada Drives collects basic customer data and sells the information to local car dealers

BANK RATING: Ally. Partners include Schedule 1 banks as well as credit unions and alternative lenders

ETHERPARTY

FOUNDER: Lisa Cheng

LAUNCHED: 2013

EMPLOYEES: 16

NICHE: Blockchain technologies

ORIGIN STORY: Head of R&D Cheng’s other company, consulting firm Vanbex Group, was paying remote workers in cryptocurrencies so often that she decided it would be easier to automate that process through a smart contract. For example, if a person makes several social media posts, that will be recognized and the person will be paid automatically according to the contract

INNOVATION: The Etherparty platform (now in beta) allows one or more parties to easily create smart contracts on blockchain networks.

BANK RATING: Ally. Etherparty is pursing partnerships with financial services firms to integrate its smart contract technology

FINN.AI

FOUNDERS: Guru Atlu, Natalie Cartwright, Jake Tyler

LAUNCHED: 2014

EMPLOYEES: 35

NICHE: Personalized digital banking

ORIGIN STORY: What started as a peer-to-peer payment company called Payso Inc. morphed into something completely different when Alberta’s ATB Financial approached the founders about creating a chatbot for clients on Facebook Messenger

INNOVATION: A personal financial management assistant billed as conversational banking, Finn.ai’s white-label app includes a natural language processing engine that allows it to converse with clients understand their questions

BANK RATING: Ally. So far, Finn has teamed up with more than 10 financial institutions on four continents. For winning the fintech and mobility category of Capgemini’s global InnovatorsRace last year, Finn.ai secured a partnership with the French IT consulting titan

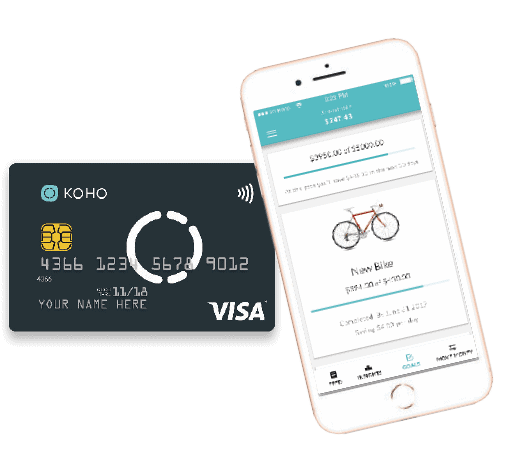

KOHO

FOUNDERS: Daniel Eberhard (above), Jonathan Bixby, Joshua Bixby, Mike Benna

FOUNDERS: Daniel Eberhard (above), Jonathan Bixby, Joshua Bixby, Mike Benna

LAUNCHED: 2014

EMPLOYEES: 15

NICHE: Mobile Banking

ORIGIN STORY: CEO Eberhard turned a university class project into a wind farm company that he sold to renewable energy titan Algonquin Power & Utilities Corp. in 2011. With Koho, he then turned his attention to taking on Canada’s banking giants, which charge some of the world’s highest user fees

INNOVATION: The Smart Spending Account allows people to pay their bills, deposit money and save, mostly without fees. Clients can make purchases with a reloadable Koho Visa card, which earns the company money through interchange fees

INNOVATION: The Smart Spending Account allows people to pay their bills, deposit money and save, mostly without fees. Clients can make purchases with a reloadable Koho Visa card, which earns the company money through interchange fees

BANK RATING: Disruptor. Besides Visa Inc., partners include Vancouver-based federally regulated financial institution Peoples Trust Co., which holds Koho customers’ money

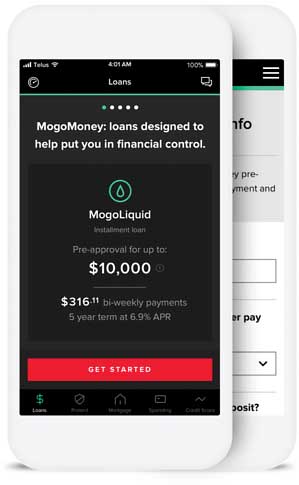

MOGO

FOUNDERS: Dave Feller

FOUNDERS: Dave Feller

LAUNCHED: 2003

EMPLOYEES: 232 (113 in B.C.)

NICHE: Online lending

ORIGIN STORY: Feller spent years struggling with debt after university, and his brother was an investment banker at Lehman Brothers Holdings when it collapsed in 2008. The resulting global credit crisis influenced Mogo’s development as faith in big financial institutions was shaken

ORIGIN STORY: Feller spent years struggling with debt after university, and his brother was an investment banker at Lehman Brothers Holdings when it collapsed in 2008. The resulting global credit crisis influenced Mogo’s development as faith in big financial institutions was shaken

INNOVATION: The Mogo app allows users to check their credit score for free, while also giving them access to a suite of financial products including mortgages, personal loans and prepaid Visa cards

BANK RATING: Disruptor. With a strong online presence plus brick-and-mortar locations, Mogo poses a challenge for financial incumbents

PAYFIRMA

FOUNDERS: Michael Gokturk

FOUNDERS: Michael Gokturk

LAUNCHED: 2010

EMPLOYEES: 30

NICHE: Payment Proessing

ORIGIN STORY: Gokturk, who has a background in investment banking, saw opportunities for innovation in the payments industry. He launched Toronto-based VersaPay Corp. in 2006, taking it public four years later. Payfirma is his second firm

INNOVATION: Payfirma was the first in Canada to introduce mobile technology that allows businesses to accept credit and debit card payments online

BANK RATING: Ally. Among the companys partners are Canadian Imperial Bank of Commerce, Canadian Western Bank and Central 1 Credit Union

RENTMOOLA

FOUNDERS: Patrick and Philipp Postrehovsky

LAUNCHED: 2013

EMPLOYEES: 24 (22 in B.C.)

NICHE: Payment processing

ORIGIN STORY: Patrick Postrehovsky came up with the idea after living in Shanghai and paying his rent with cash off his credit card and racking up points. On returning to Canada, he decided to develop a service for renters and landlords that would reduce the costs of cheque and cash processing

INNOVATION: Pioneered credit card payments in the Canadian property management space by allowing renters to pay their rent with plastic. The service is available in 400 North American cities

BANK RATING: Ally. Partner bank is BMO Financial Group

VENZEE

FOUNDERS: Kate Hiscox (above) and Marco Sylvestre

LAUNCHED: 2014

EMPLOYEES: 41

NICHE: Connectivity and data transformation

ORIGIN STORY: Chief executive Hiscox started Venzee after realizing there was a market for a cloud-based inventory management system for retailers, suppliers and manufacturers

INNOVATION: Venzee’s Mesh platform connects everyday apps and enterprise solutions with blockchain networks (users that each have to agree on all transactions coming in and out). Features include custom smart contracts, data transformation and failsafe conditions that remove or encrypt sensitive data before committing to a blockchain network

BANK RATING: Ally and disruptor. Banks can use Mesh, but the platform also makes alternative currencies more viable and accessible for the average consumer

VOLEO

FOUNDERS: Jay Sujir, Mark Morabito, Thomas Beattie

LAUNCHED: 2013

EMPLOYEES: 13 (5 in B.C.)

NICHE: Online investing

ORIGIN STORY: Sujir, a Vancouver lawyer, came up with the concept of developing smart phone apps for groups of investors to work together in the wake of the 2008-09 financial crisis when faith in advisers was shaken. The idea is beginning to take off. Last year the company went through the prestigious Accenture FinTech Innovation Lab and was named Best of Show, along with Finn.ai, at the FinovateFall tech show in New York

INNOVATION: The Voleo social trading app lets a number of investors pool money and time to work together and establish a group portfolio. It also makes it easier for novice investors by offering tools to help them learn and gain confidence

BANK RATING: Ally and disruptor. Banks may be involved in the investing process, but some of the services banks traditionally offer (i.e., investment advice) aren’t required.