Real estate developers face a combination of mounting debt and sagging demand for new homes. The broader B.C. economy could feel the pinch, too

Although B.C. has arguably been the biggest beneficiary of the most recent housing boom, a tidal wave of cheap money has flooded across the nation and into the hands of real estate developers desperately trying to keep up with a home-buying frenzy. Thanks to their efforts, housing starts hit record highs, and so did bank loans.

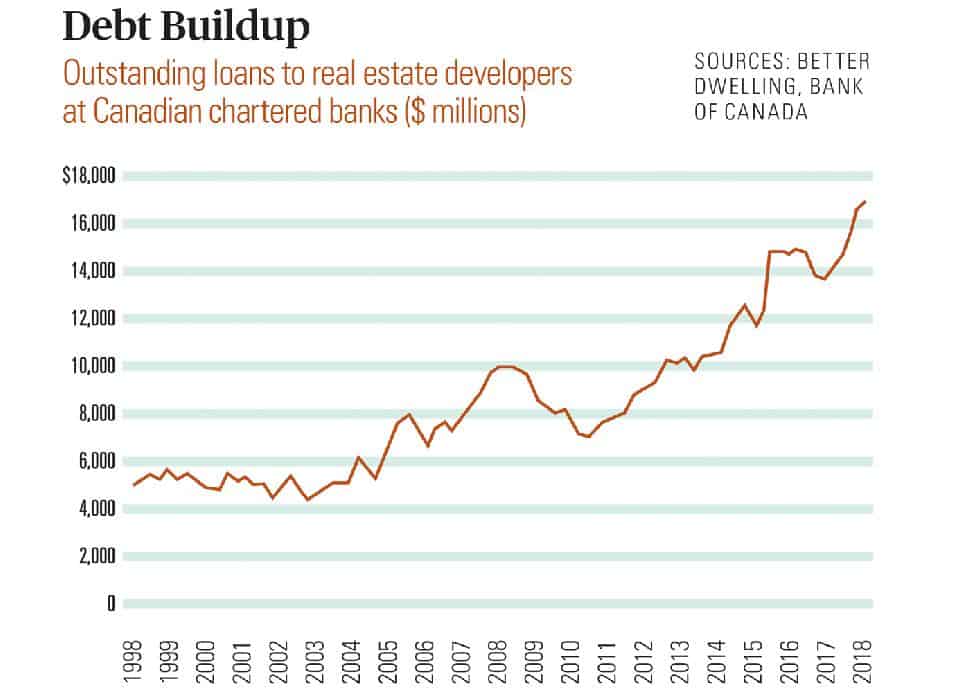

Canadian real estate developers are borrowing more than ever, the Bank of Canada reports. Their outstanding loans reached $16.68 billion in the fourth quarter of 2018, up 2.36 percent from the previous one. This represents a 20.28-percent jump compared to the fourth quarter of 2017.

Meanwhile, following a raft of government measures aimed at reining in runaway household debt and property prices, demand for new homes has hit the skids. Still, a record number of residences remain under construction, with their builders all aiming to cross the finish line so they can pay off loans.

Property developers in B.C. face increasingly tough conditions as provincial taxes, along with the retreat of Chinese capital flows, have put even more downward pressure on the housing sector. The latter is of particular concern, given recent Canada Mortgage and Housing Corp. figures suggesting that non-resident buyers make up a much larger segment of the new construction market than previous estimates showed.

In Vancouver, 19.2 percent of condominiums built from 2016 to 2017 had at least one non-resident on title, the CMHC notes. The proportion is even higher in other B.C. cities. For condos built in Coquitlam during that period, 20.8 percent fell into the same category, according to urban planner Andy Yan in the Globe and Mail. In Surrey, the total is 20.5 percent; it’s 25.1 percent in Burnaby, and a whopping 25.8 percent in Richmond.

With non-resident purchasers pulling back, it should be no surprise to see many developers offering increased buyer bonuses and incentives on recently launched projects.

The slowdown in the new property segment must be keeping developers and bankers up at night, but further deterioration could have a much broader economic impact. As of 2018, 9.5 percent of the B.C. labour force worked in construction, according to Statistics Canada, and real estate and construction services make up more than 25 percent of provincial GDP. Also, last December, new home sales accounted for 11.5 percent of all transactions at the Land Title and Survey Authority of British Columbia.

Whether you’re a banker, a builder or someone in a different line of work, the development space remains as crucial as ever to the provincial economy.