Wayne Deans, Deans Knight Capital Management | BCBusiness

One of Vancouver’s more colourful money managers, Wayne Deans is known to dress loudly, laugh easily and swear fluently.

At best, Vancouver is an afterthought in the world of finance, a distant contender behind London, Hong Kong and New York. Yet the city boasts a stellar cast of money managers who oversee some of the biggest funds in Canada and consistently beat the averages. Maybe it’s something in the water. Or just a love of all things green.

As a Vancouver investment manager, Wayne Deans works in the import business. “There’s not much money here,” says the chair and CEO of Deans Knight Capital Management Ltd. from across the blond-wood table of his 15th-floor downtown boardroom, which offers floor-to-ceiling views of Burrard Inlet and the North Shore Mountains. “So if you’re going to be an investment management firm here, you’ve got to be prepared to go somewhere else and get the money.”

Like some of his local peers, Deans is adept at winning capital from across Canada and around the world. A specialist in managing wealth for the super rich, he’s got the Ferraris to prove it. “We’re an international firm,” Deans says. “We just happen to be here. We could do what we do from anywhere.”

Maybe so, but Vancouver punches above its weight when it comes to homegrown investment firms. During the past several decades, the city’s money managers have built a diverse and thriving industry that’s earned the trust of everyone from B.C. clients to the globally wealthy and big foreign pension funds. A few of them have long-term performance numbers that would raise eyebrows in New York, London and, heaven forbid, Toronto.

The city is home to Phillips, Hager & North Investment Funds Ltd., a key division of Canada’s largest investment house. It’s also spawned investors with world-beating track records – and the country’s biggest independent money manager, Connor, Clark & Lunn Financial Group Ltd. On top of that, a growing number of traders and analysts on Wall Street and elsewhere got their start here.

None of this happened by accident. The Vancouver investment industry owes much of its strength to a handful of local pioneers. Founded in 1964 by Art Phillips – who later became mayor – Bob Hager and Rudy North, PH&N started with just $3 million in capital. Royal Bank of Canada bought the firm in 2008; by then it managed close to $70 billion in assets.

The early 1980s saw the launch of three other pivotal shops: Connor, Clark & Lunn, Leith Wheeler Investment Counsel Ltd. and M.K. Wong & Associates. The latter was co-founded by the late Milton Wong who, with Leith Wheeler principal Murray Leith Sr. and others helped establish the Portfolio Management Foundation program at UBC’s Sauder School of Business, a rich source of talent. And like PH&N, M.K. Wong spun off several local startups. Thanks to this remarkable legacy, a second generation has flourished and a third one is asserting itself.

Known as a bond trading centre, Vancouver has some star performers in the alternative investment space, too. Take $1.3-billion-plus Vertex One Asset Management Inc.: founded by a trio of M.K. Wong alumni, it runs one of Canada’s biggest and most successful hedge funds. Its Vertex Fund and PH&N’s Absolute Return Fund were two of just three Canadian offerings to make Barron’s list of the 100 top-performing global hedge funds for 2009 through 2011.

Past performance is no guarantee of future results. But here’s what several of Vancouver’s leading investment pros have to say about where their industry came from, how it works – and what it could become.

[pagebreak]

Larry Lunn launched his firm with the help of

advice from Bob Hager; “I”m looking around

for the next Art Phillipses and Bob Hagers and

Milt Wongs,” he says.

Larry Lunn

Connor, Clark & Lunn Financial Group Ltd.

When Larry Lunn decided to launch his own firm in 1982, Phillips, Hager & North co-founder Bob Hager took him for a three-hour lunch. “He told me a whole bunch of things that I needed to do to have some initial success in the business,” says the chair, president and chief investment officer of Connor, Clark & Lunn Financial Group Ltd.

“I said, ‘Bob, why are you doing this?’” continues Lunn, whose boyish features and rectangular eyeglasses give him the air of a watchmaker. “And he said, ‘The more people we have here that are successful, the better it is for our community and all of us.’”

After working at financial firms in Toronto, Calgary and Montreal in the 1970s, Lunn moved to Vancouver, where he opened Connor, Clark & Lunn with backing from his two Toronto-based partners: John Clark, who has since retired, and Gerry Connor, now chair and CEO of Cumberland Private Wealth Management Inc. He went into business for himself because he thought the local market was underserved, but at first he battled the perception that most money management wisdom emanated from Toronto. So he travelled to Hogtown, where his pitch to pension funds was that his firm offered an alternative to Bay Street groupthink. That approach paid off, and the firm’s eastern cred helped it win business in the West.

In 1987, CC&L made its name by anticipating that year’s equity market crash. Over the next five years, its assets climbed from $700 million to $5 billion. It now manages some $43 billion for institutional and individual investors, under a “multi-boutique” model, with stand-alone investment affiliates backed by centralized distribution and business management.

Although the 273-employee CC&L’s corporate arm is centred in Toronto, much of its money management and administrative services remain in Vancouver, says Lunn, who serves as group chair and heads the risk management committee. Besides other Canadian locations, the firm has a small London office.

Fifteen years ago, independent firms dominated the local investment industry, Lunn notes. “Today if you look at the top 40 firms, it’s concentrated in large international players and the banks,” he says. “And so there’s people who are worried that it’s become overly institutionalized.”

Lunn, who has no plans to retire, contends that CC&L will always keep a big local presence. “I don’t get a sense that there’s a groundswell to start new businesses and really go after the market,” he says disappointedly of Vancouver. “I’m looking around for the next Art Phillipses and Bob Hagers and Milt Wongs.”

Still, Lunn admits that the world has changed for investment startups. “You need such sophisticated systems and governance structures,” he says. “It’s so much more difficult today to do what we did 30 years ago.”

Tom Bradley set out to build the anti-

establishment fund company, with low expense

ratios, minimal holdings and portfolios that

ignore the indexes.

Tom Bradley

Steadyhand Investment Funds Inc.

If Vancouver money managers work away from the crowd, Tom Bradley takes things a step further. His firm’s modest ground-floor premises are on a leafy street in Kitsilano, with a motor scooter bearing the Steadyhand logo parked out front.

Something of an iconoclast in the Canadian investment business, the tall, mop-topped Bradley is a devotee of the irreverent Fox TV series Family Guy. “For me, it’s helped,” the Steadyhand president says of managing money from Vancouver. “I think I have been able to disengage from the Bay Street model.”

When Bradley and co-founder Neil Jensen launched Steadyhand in 2007, they set out to shake up a mutual-fund industry that has earned a reputation for flogging mediocre products and nickel-and-diming investors. Rather than selling its six funds through financial advisers, the firm offers clients direct access with low base fees (between 0.65 and 1.78 per cent) and no hidden costs.

Although Bradley runs the Founders Fund, which launched in 2012, outside managers from Canada and Europe handle the other five. Steadyhand’s four-point investment philosophy is solid: concentrate on 20 to 30 stocks, build a portfolio that bears no resemblance to the index, let managers do their thing and keep asset turnover low. Steadyhand now has a respectable five-year record. With an 8.4 per cent compound annualized return through last September 30 since its February 2007 inception, the firm’s top performer is the $29-million Small-Cap Equity Fund managed by Montreal-based Wil Wutherich.

“Five-year performance is really important in our business and we’ve played that up to the hilt,” says the plainspoken Bradley, who’s been adept at publicizing $210 million-in-assets Steadyhand, partly through his Globe and Mail column. “People are going, ‘Oh, I guess it works. What Tom has been preaching actually works.’ ”

The 57-year-old Winnipeg native brings plenty of experience to the task. Bradley opened Steadyhand two years after quitting as president and CEO of Phillips, Hager & North, where he’d worked since the firm recruited him to Vancouver in 1991. Previously, the University of Western Ontario MBA grad had been head of national institutional equity sales at Richardson Greenshields in Toronto. “I stepped onto a rocket ship,” Bradley says of PH&N, where he took the reins in 1999, referring to its track record and its profitable pension business. “My legacy there was probably just saying, ‘Hey, we’ve got something here. Let’s build it.’ ”

Steadyhand, whose nine staff include one in Toronto, does roughly 45 per cent of its business in B.C., with another 45 per cent coming from Ontario and the rest from the Prairies. Bradley has multi-billion-dollar ambitions. “Where we’re different from some of the other startups in town is we’re trying to build a scalable national business from scratch,” he says. “It might take another five years before we’re at the tip of somebody’s tongue, but I think we have that shot.”

[pagebreak]

John Montalbano

RBC Global Asset Management/Phillips, Hager & North Investment Management

John Montalbano doesn’t buy the argument that Vancouver’s investment business is losing its autonomy. “I completely disagree with that view,” says the chief executive of RBC Global Asset Management and Phillips, Hager & North, which Royal Bank of Canada acquired for $1.4 billion in early 2008. “When we did the deal with RBC, some of our competitors unfortunately would throw out the comment that decision-making would be east, and nothing could be more wrong.”

Yes, RBC Global Asset Management chief investment officer Daniel Chornous lives in Toronto. But Montalbano has some numbers to support his case. Since the RBC takeover, PH&N has grown its local staff by about 20 per cent, to 239. And despite the credit and euro crises, the firm’s assets have swelled more than 37 per cent to $93.6 billion, all of it managed from Vancouver.

Montalbano is also proud of the national recognition that PH&N has gained. For the past three years, it’s won the Best Overall Fund Group and Best Bond Fund Family categories at the Canadian Lipper Fund Awards.

For Montalbano, 46, the biggest risk facing the local industry is a dearth of managers who can meet clients’ increasingly sophisticated needs. “Most of the investment community in Vancouver is geared to manage local investments. And they haven’t made the investment to be in a position to do alternatives or global investing,” says the frequent visitor to Europe, Asia and Latin America.

Montalbano was born in Yellowknife and attended UBC, where he won a spot as one of eight students in the inaugural Portfolio Management Foundation class of 1987. The program lets students manage a portfolio of real money and work with mentors from throughout the Vancouver investment community. That’s how Montalbano met Milton Wong, whom he considers one of his most important mentors. He then got a summer job at PH&N with co-founder Art Phillips and the two went on to share a desk for almost 13 years. Named president of PH&N in 2005 after the departure of Tom Bradley, Montalbano was previously a U.S. equity analyst and ran the firm’s institutional client relationship team.

PH&N serves a largely institutional clientele and 80 per cent of its assets are from outside B.C. But Montalbano sees an opportunity to cater to super-rich immigrants from Eastern Canada and abroad. “That will be something that most of us in Vancouver will have to orient ourselves toward,” he says, “To make sure that we’re relevant not only to the Canadian who’s immigrating to Vancouver but also the global immigrant who’s not looking for a lot of Canadian solutions.”

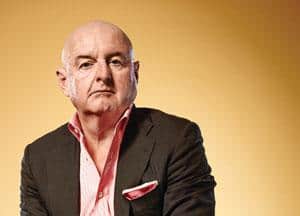

Wayne Deans and Craig Langdon

Deans Knight Capital Management Ltd.

For Wayne Deans, working on the West Coast has its drawbacks. “Because our clients are so spread out, our travel schedule is the most difficult,” says the Deans Knight co-founder. “We’re like the Canucks.”

Dressed in jeans and a form-fitting red-and-white striped shirt with a high collar and no tie, Deans laughs easily and swears fluently. “The upside – I’m not sure it’s as true today as it once was – is that you have the luxury of being able to think more independently here,” says the Montreal native, whose fingers flash with chunky silver rings. “We never see the rest of the financial community. If you’re in Toronto, you’re all drinking in the same bars, you’re all going to the same seminars, you’re all going to the same road shows and you’re all drinking the same bathwater.”

With $1.3 billion under management, Deans Knight serves a few pension funds and foundations. But its focus is what Deans calls ultra-high net worth individuals and families, some of whose wealth is in the billions. The firm has clients in Calgary, Montreal and Toronto, but also throughout the U.S. and Europe.

Deans Knight has two main investment strategies: income and capital growth. Two-thirds of its capital is in stocks – the growth side of the business – and the rest is devoted to income. “We’re highly concentrated in 15 to 20 businesses and that’s unique when you start to look at other companies around,” explains Deans Knight president and co-chief investment officer Craig Langdon of the firm’s stock investments. On the income side, Deans Knight was the first Canadian specialist in high-yield corporate bonds, also known as junk bonds.

Deans, 66, started out in the securities department of the Bank of Canada in Ottawa after earning an MBA from McMaster University. The central bank dispatched him to Vancouver from 1976 to 1978; he returned east to work at Wood Gundy in Toronto, then returned to Vancouver in 1985 when his friend Milton Wong recruited him to M.K. Wong & Associates.

Fired by Wong in 1992 over what he describes as an ownership fight, Deans launched Deans Knight with M.K. Wong co-founder Doug Knight, who has since left the firm. Starting with pension and mutual fund business, Deans and Knight eventually found their niche in private wealth. The firm’s flagship DK Equity Growth Fund has been volatile over the years, but has delivered extraordinary long-term performance. Through last September 30, the fund had posted a 15.8 per cent annualized return since its 1993 inception, compared to 8.8 percent for the S&P/TSX Composite Index. Deans can sound boastful about his firm’s successes, but he’s also disarmingly frank when it comes to missteps. Over its 20-year life, Deans Knight has only had a couple of dozen wildly profitable investment plays, he estimates – typically take-outs after a struggling business it owned big stakes in got turned around. “If you’re not making mistakes, you’re probably not making enough decisions,” Deans says. “You’re not taking enough risk.”

[pagebreak]

Murray Leith

Odlum Brown Ltd.

The son of the late Murray Leith Sr., co-founder of Leith Wheeler Investment Counsel, Murray Leith grew up with shoptalk around the kitchen table. Liking what he heard, Leith earned a commerce degree in finance at UBC and spent several summers working at his father’s firm. He began his career in 1990 as an analyst at Vancouver-based McDermid St. Lawrence Securities, which later merged with Goepel Shields & Partners before Raymond James Financial Planning Ltd. acquired the new firm.

In 1994, Leith jumped at the chance to become director of research at Odlum Brown, B.C.’s second-oldest independent investment dealer. He liked the fact that his new employer focused on wealth management for conservative investors and invested in big companies. “That was a glove that fit a lot better for me,” recalls the 46-year-old Odlum Brown vice-president, who leads a six-member research team. “The firm always had a value focus, and that was my background.”

In his first year, Leith created the Odlum Brown Model Portfolio, a hypothetical equity portfolio that typically holds 40 to 50 large-cap stocks. “Initially the idea was that the average money manager, the average mutual fund in the country doesn’t beat the market,” he says. “So I thought, ‘Well, why don’t we put together a portfolio that has good odds of doing better than the market?’ ”

Leith and his team stayed close to the sector weightings of the benchmark TSX/S&P Total Return Index – but they set out to beat the index by picking the best companies. The results have been impressive. As of last September 15, the Model Portfolio had posted a 14.9 per cent compound annual return since inception, versus 8.8 per cent for its benchmark.

Odlum Brown, which was established in 1923 and manages some $7.2 billion, mostly for local and other Canadian clients, never turned the Model Portfolio into a mutual fund. But some clients and their advisers follow it almost trade for trade through segregated accounts, while other advisers and portfolio managers use it for investment ideas, says Leith, who is an avid boater, skier and cyclist. “In addition to providing a portfolio that people can replicate, it’s meant to give some context to individual stock recommendations, what sort of weighting they should be in an overall portfolio.”

For the past five years, about 45 per cent of the Model Portfolio has been in big foreign companies with strong balance sheets, explains Leith. He says diversification away from Canadian names is finally paying off.

Leith concedes that being in Toronto or New York would make it easier to cover stocks such as financials. “But normally when we initiate coverage on a company, we go out and visit, kick the tires, see the factory, establish a relationship with management,” he says. “Once you’ve done that, you don’t always need to be in front of them.”

Victoria native Jonathon Palfrey could have

made his fortune in Toronto but chose to stay

in B.C., honing his skills at the firm founded

by local legends Murray Leith Sr. and Bill

Wheeler.

Jonathon Palfrey

Leith Wheeler Investment Counsel Ltd.

As Jonathon Palfrey describes it, a strong and growing Vancouver investment industry was overshadowed from the 1960s through the 1980s by Howe Street and its parade of colourful characters. “This more conservative world of discretionary money management existed at the same time,” says the Leith Wheeler senior vice-president and portfolio manager as he sits in a boardroom 15 floors above Burrard and Pender streets. “It just didn’t get all the headlines.”

Palfrey could have sought his fortune in Toronto or elsewhere, but he chose Vancouver. Raised in Victoria, he earned a commerce degree at UBC and spent six years in the mortgage industry before joining Leith Wheeler in 1996. A shareholder in the business for 15 years, he runs its private client and foundation practice.

Launched in 1982 by Murray Leith Sr. and Bill Wheeler, who were both investment analysts, Leith Wheeler started by serving private clients. Today, pension funds account for about $10 billion of its roughly $12 billion in assets. The firm has a national client base that includes Toronto pension plans and foundations.

Palfrey describes Leith Wheeler as a low-profile outfit that aims to grow by no more than 10 per cent annually. “If you have too many institutional assets, you can outgrow the Canadian marketplace,” says the 45-year-old, who has perfect teeth and the chiseled good looks of an action figure. “The bigger you get, the tougher it is to be different from the market.” With that in mind, Leith Wheeler has expanded carefully by closing parts of its business to new capital.

The 60-employee firm, which opened a Calgary office in 2011, manages balanced portfolios of bonds and Canadian and U.S. equities. It runs the bonds and Canadian equities in-house but uses Toronto-based Sprucegrove Investment Management for foreign stocks.

As a bottom-up value manager, Leith Wheeler has a disciplined investment process that has worked in all kinds of markets, Palfrey explains. “Maybe investors can get a little bit short-term focused when the outcome is so uncertain,” he says of recent conditions. “But we still believe in a balanced, diversified portfolio being able to make reasonable returns above inflation over time without making some wild, crazy bets.”

The fact that Vancouver is an attractive city has helped Leith Wheeler make recent hires from London and San Francisco, Palfrey says, adding that the opportunity to be a partner in an employee-owned company is an inducement too. The firm often recruits Vancouver natives who have worked somewhere else, but the high cost of living means that they tend to be in the middle of their careers.

[pagebreak]

Hanif Mamdani

RBC Global Asset Management/Phillips, Hager & North Investment Management

“I am a value investor,” says Hanif Mamdani, a serene-looking man in a charcoal suit and a blue, open-necked shirt. “To beat the market and to generate good returns, you have to buy things that are fundamentally underpriced or mispriced,” explains the head of alternative investments at RBC Global Asset Management and Phillips, Hager & North. “It sounds obvious, and yet it’s remarkable how many times people don’t put those words in practice.”

One of Canada’s smartest investors, Mamdani, 46, could have been a rocket scientist – literally. Born in Kenya, he grew up in Burnaby and earned his engineering degree at the California Institute of Technology, where he did computer programming for a professor who worked at Caltech’s Jet Propulsion Laboratory, a NASA research centre. Admitted to graduate programs at Harvard University, the Massachusetts Institute of Technology, Princeton University and Stanford University, Mamdani chose to pursue a master’s in applied science at Harvard.

But after graduating in 1988, he spent a decade on Wall Street, where he worked in equity capital markets at Credit Suisse and became head of convertible bond trading at famed investment bank Salomon Brothers. In 1998, shortly after Salomon agreed to become part of Citigroup, Mamdani came back to Vancouver. He had the good fortune to meet PH&N’s then-president Tony Gage, who introduced him to the fixed-income team.

Mamdani started at PH&N as a credit analyst and became chief investment officer before RBC bought the firm in 2008. Today he does all of the trading on the $3.3-billion High Yield Bond Fund and the $735-million Absolute Return Fund. He also helps oversee the investment-grade corporate bond team, which manages $20.4 billion.

Since its 2002 launch, the Absolute Return Fund had earned an annualized 14.7 per cent net of fees as of last October 31. Mamdani uses several hedging strategies in the fund. One is pairs trading, which involves buying two stocks in the same industry – one cheap and one overpriced – shorting the latter and waiting for a reversion.

For five of the past six years, Morningstar Canada has ranked the High Yield Bond Fund as the country’s best such fund. And in 2011, Investment Executive magazine named Mamdani Canada’s fund manager of the year. He’s quick to credit his team for this success. “We live pretty modestly, all things considered,” adds Mamdani, who keeps a long row of investment books on his tidy desk. “This is not a firm where money dominates the culture.”

Mamdani believes Vancouver has potential as a hedge fund centre, provided it can build a critical mass of investment talent, along with accountants, lawyers and other professionals to service the industry. “In the same way that San Francisco has become a terrific investment hub for international equity management, Vancouver could easily become a mini hedge fund Mecca.”

He also thinks the city’s investment community would benefit from greater intellectual output. “What we really want to see in Vancouver are more decision makers who actually construct investment portfolios,” he says. “For this city to become a hub, we need more of that investment manufacturing – real investing happening here in Vancouver.”