B.C. and the rest of Canada could be at risk of a deflationary spiral that would hurt more than home prices

Central bankers worried about Canada’s economic health should listen to top U.S. hedge fund manager Ray Dalio. “Typically the worst debt bubbles are not accompanied by high and rising inflation, but by asset price inflation financed by debt growth,” the Bridgewater Associates founder writes in his recent book, Principles for Navigating Big Debt Crises. “Central banks make the mistake of accommodating debt growth because they are focused on inflation and/or growth—not on debt growth, the asset inflations they are producing, and whether or not debts will produce the incomes required to service them.”

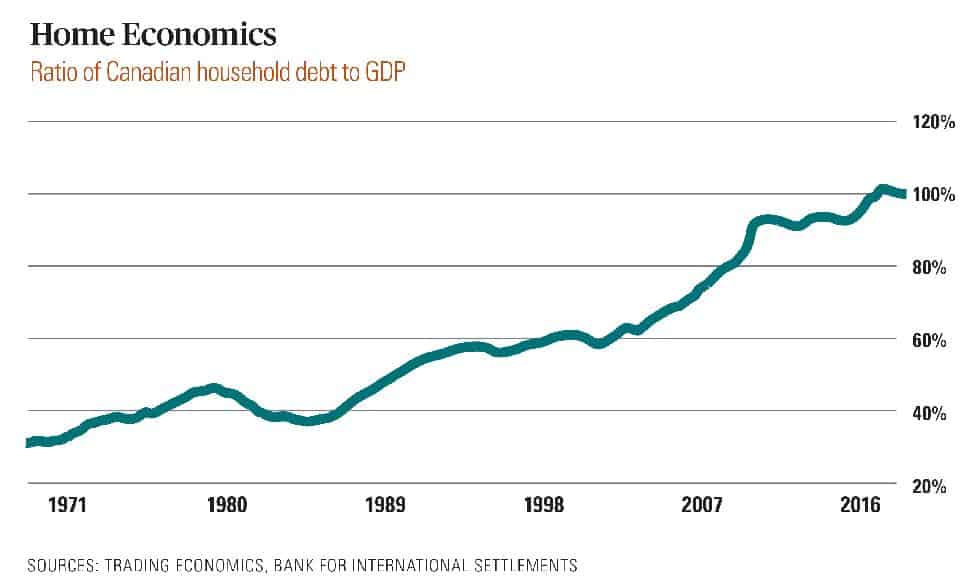

Look at Canada, where the central bank is aggressively hiking interest rates and private debt has expanded by 20 percent in five years, according to the Swiss-based Bank for International Settlements, the most for any advanced economy. The nation’s ratio of household debt to GDP now sits at a record 100 percent.

Low interest rates, combined with an expansion of credit, have helped push residential property prices to all-time highs. As of September, the average sale price for a home in Canada was $486,917, the Canadian Real Estate Association (CREA) reports. The average sale price of a B.C. home that month was $685,749.

Citing concerns over rising inflation and an economy nearing capacity, though, the Bank of Canada has kept its foot on the gas pedal lately, hiking interest rates five times in just over a year. Unsurprisingly, this has choked off credit growth and dented home sales.

In September, sales fell year-over-year in 70 percent of local markets, mostly led by major B.C. urban centres, the CREA notes. This slowdown also sent housing starts to a 19-month low after declines in four of the previous five months, according to Canada Mortgage and Housing Corp.

Overindebted households hit with rising borrowing costs pushed the debt service ratio— the share of income servicing interest and principal on mortgage, credit card and other debt—to 14.2 percent in the second quarter, Statistics Canada indicates. That’s the highest level since the end of 2008.

But the knock-on effects are much broader. Not only has housing cooled, but auto sales, another rate-sensitive industry, have been hit hard. Canadian purchases of new light vehicles dipped 7.4 percent year-overyear in September, Ontario-based DesRosiers Automotive Consultants notes, the largest monthly drop since 2009.

All of this adds up to a slowing Canadian economy where the most indebted households in the G20 face interest-rate hikes and burdensome payments. Some observers worry that the country will suffer a household deleveraging where home prices fall as consumers pay down debt, creating a deflationary spiral. Such a problem can get worse when the central bank has little room to cut interest rates.

Dalio’s advice: “The best way of negating the deflationary depression is for the central bank to provide adequate liquidity and credit support, and, depending on different key entities’ needs for capital, for the central government to provide that too.”

What does it all mean for B.C. real estate investors? At this stage of the debt cycle, they’d be smart to seek out properties with sustainable cash flow that can weather a potential downturn. In other words, save the speculation for another day.