As Vancouver’s detached home market grinds to a screeching halt, could the provincial economy follow?

The real estate boom gripping B.C., and the city of Vancouver in particular, has been historic on nearly all fronts. The frenzy to snatch up Vancouver soil kicked off in 2013. Bidding wars for detached homes spread like wildfire, pushing sales to a record in 2015, along with dollar volumes, which hit $8.9 billion that year, according to the Real Estate Board of Greater Vancouver. The average sale price of a detached home in the province’s largest city surged 48 percent from 2014 to 2016, reaching an all-time high of $2,825,858.

In response to public angst about runaway housing costs, policymakers at all levels dog-piled onto the real estate market, announcing a foreign buyers tax, two mortgage stress tests and a hike in the property transfer tax, to name a few measures. Meanwhile, the Chinese government took swift action to curb capital outflows, requiring citizens to pledge that they wouldn’t use cash leaving the country to buy property. Outflows from China plunged 67 percent last year, according to investment firm Pictet Wealth Management.

As a result, multiple offers vanished and speculative activity dried up, leaving would-be house flippers facing a liquidity crunch.

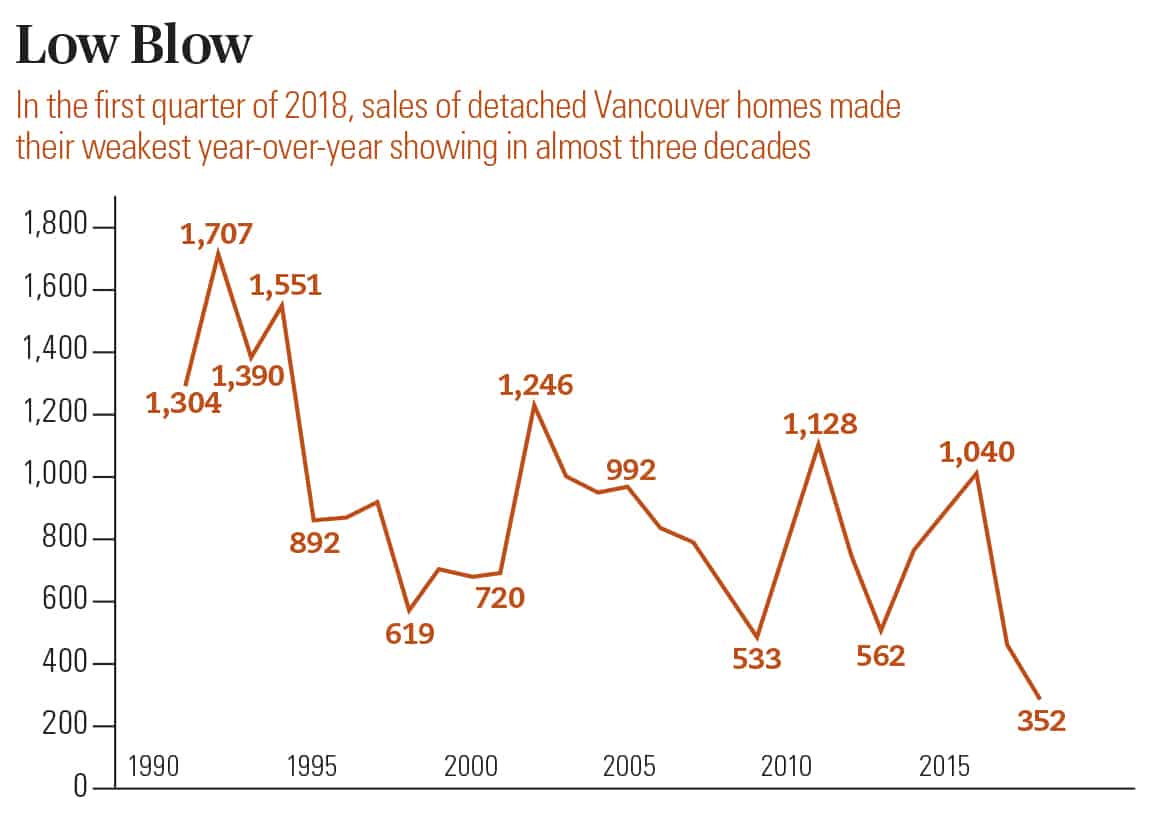

Many sellers remain willfully optimistic about a rebound in 2018, but it hasn’t been the start they were hoping for. In the first quarter, Vancouver detached home sales fell to their lowest for that period in more than 27 years.

Increased taxation has pushed foreign bids to the sidelines, with a $3-million purchase now requiring those buyers to cough up $668,000 in levies upon closing. Local purchasers have been stymied by rising mortgage costs and tougher qualifying rules. A typical Vancouver household with an average mortgage would have to part with an additional 9 percent of its income to service a 1-percent rise in interest rates, the National Bank of Canada estimates.

With rates expected to keep inching upward in 2018 and the provincial government intent on curbing house prices, a quick rebound in Vancouver’s detached home market could be a fading pipe dream. Now it’s become apparent that banks have started pricing in additional risk, raising borrowing rates and getting more selective about who qualifies for a loan. Homeowners hoping to renew their mortgages are also at the mercy of their current creditors following new B-20 mortgage guidelines that require borrowers to face a stress test if they want to switch. This allows lenders to squeeze them when it comes time for renewal, especially if credit conditions continue to erode.

Such headwinds leave the B.C. economy, especially its real estate and construction industry, in a vulnerable position. The sector now comprises almost 25 percent of provincial GDP, Statistics Canada estimates. With some 55,000 housing units under construction, nearly double the long-term average, it’s been firing on all cylinders. Unless you’re hoping for a crash, it could be time to think about taking shelter.

Sources: Real Estate Board of Greater Vancouver